The International Energy Agency (IEA) released its latest special report last week, entitled ‘The Role of Gas in Today’s Energy Transitions’. The report is somewhat incoherent in the way it deals with the controversial role of gas in the climate crisis.

The incoherence manifests in a couple of ways. For an IEA report, it is uncharacteristically cautious about the long-term future of gas. But it then makes a concerted pitch for increased gas consumption. It reveals the impotence of gas as a climate solution, while still insisting that gas can help reduce emissions.

More typical is the report’s analytical flaws that adhere to the IEA’s mantra on the persistent role of gas and fossil fuels in a clean energy future. These include:

- relying on flawed government data on methane leakage to underplay the climate impact of gas;

- insisting that carbon capture and storage will enable the continued expansion of the fuel’s energy market share (any day now!);

- assuming that the oil and gas industry will one day see the light and do everything possible to reduce preventable pollution (don’t hold your breath);

- presenting carbon pricing as the primary regulatory response, and;

- vastly understating the urgency of the climate crisis.

There’s a lot there. This blog post is the first of three critiquing the claims in this new IEA report. Let’s start with some of the positive aspects. (Part 2 is here)

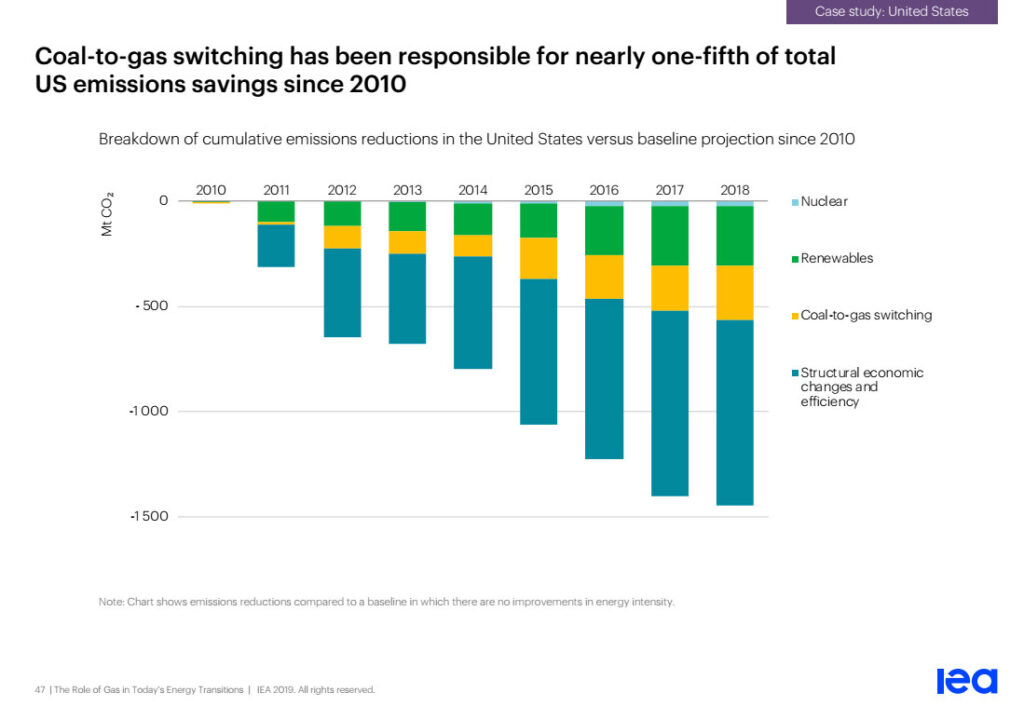

IEA shows that coal-to-gas switching is least responsible for recent declines in power sector emissions. Renewables and efficiency clearly do more to cut emissions.

The report cedes a lot of ground on the very limited impact gas has in reducing greenhouse gas (GHG) emissions. This is surprising for the IEA, as it has for years promoted gas as the cleanest fossil fuel. It continues to project growth in gas production and consumption in all its energy scenarios, including its supposedly Paris compliant one, the SDS (Sustainable Development Scenario). But the facts are the facts, and it’s good to see the IEA presenting this data.

Right up front in the executive director’s foreword, Dr. Fatih Birol states that, “(gas) can bring environmental benefits, but it remains a source of emissions in its own right and new gas infrastructure can lock in these emissions for the future.” (emphasis added) This is an unusual admission for Dr. Birol, who is often in the media encouraging greater investment in oil and gas production and the infrastructure to support it. Lock-in is one of the five reasons we discuss in our bridge fuel myth busting report for why we must stop building new gas infrastructure. Unfortunately, the report only pays lip service to this important concept.

However, a key finding of the report shows how limited the impact of coal-to-gas switching has been. The first sign of this is in the Key Findings section on page 8. The report notes that while global energy-related CO2 emissions were generally flat in the three years leading up to 2017, growth resumed in 2017 and 2018.

The report states that emissions could have been a full 7 gigatons (Gt or billion metric tons) higher in 2018 if it weren’t for, “changes in the global economic and energy system since 2010: these include reductions in the energy intensity of the world economy, in part due to greater efficiency, as well as reductions in the carbon intensity of the energy sector related to the rise of renewables and switching to less carbon-intensive fuels.” The stated contribution of coal-to-gas switching in this 7 gigaton saving is 500 million tons, or about 7%.

Note that these numbers are based on the IEA’s assessment of lifecycle emissions for coal and gas-fired power generation. These assessments are based on flawed estimates of methane leakage and the relevant measure of methane’s climate impact. We will deal with this accounting issue in a subsequent post. But it is crucial to note that even with these flawed lifecycle emissions estimates, it is clear that the impact of gas on reducing emissions is far less than many in industry and government have claimed.

The chart below, copied from the U.S. case study (page 47), shows how this has played out in the country that has done the most coal-to-gas switching since 2010. Coal-to-gas switching unsurprisingly had a bigger impact here than the global average. But it was still responsible for less than 20% of emissions reductions compared to a projection from a 2010 baseline.

In fact, while the IEA does not provide the figures for the renewables contribution, it looks in the chart that in most years renewables had a greater or roughly equal impact. It is also clear that it is structural economic changes* and efficiency that had by far the greatest impact.

This might come as a surprise to the folks over at the American Petroleum Institute who never seem to tire of portraying gas as, “the biggest reason why levels of carbon dioxide in the air are the lowest they have been in nearly 25 years.”

The finding is crucial to understanding why we must challenge the myth of gas as a climate solution at every opportunity. While hundreds of billions of dollars are poured into fracking, pipelines and LNG infrastructure, it is efficiency and renewable energy that are the key to reducing emissions. Accounting for methane leakage has always made this clear. But this analysis, which underestimates the impact of methane, makes clear that with or without excessive methane leakage, gas is the least effective solution.

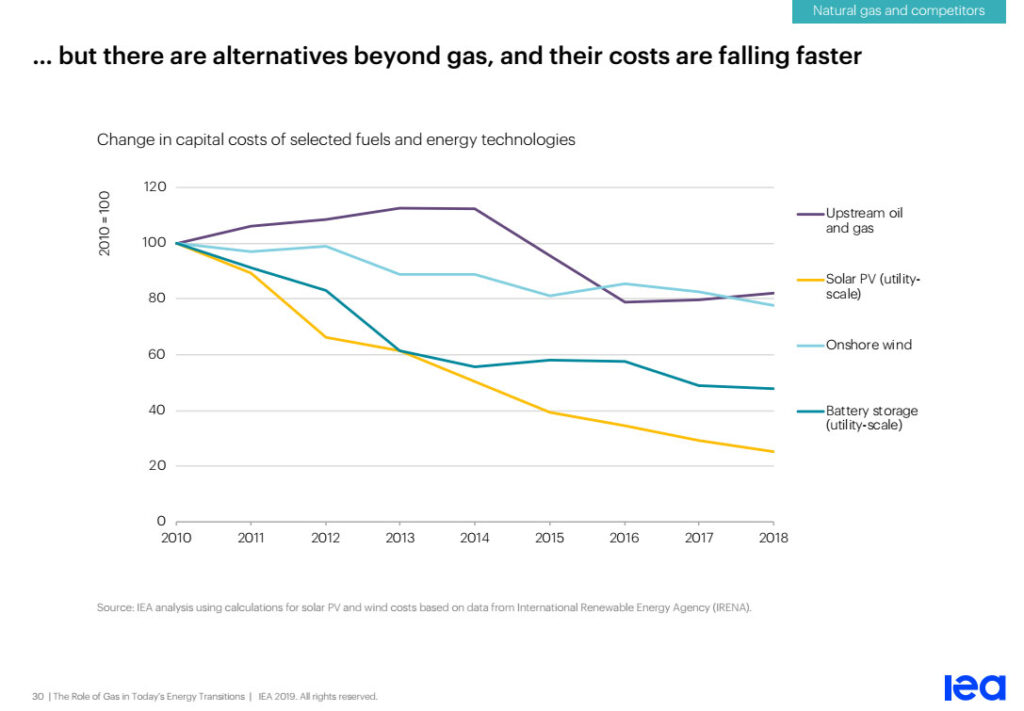

The report confirms that renewables are beating gas on cost, battery storage is next, and there’s no case for building new gas power plants.

The report confirms a trend that we have documented for the past two years, and one that is now almost universally recognized in energy circles. It’s now cheaper to build and operate utility scale wind and solar plants than it is to build and operate a gas power plant. This trend will continue and the economic case for building new gas plants has crumbled. This is not just a trend in the rich economies of Europe and North America, but also in China and India.

The chart from page 30 only partially tells the story. It compares the decline in costs since 2010 of solar, onshore wind, and battery storage with the cost of producing oil and gas.

In the Europe case study, the report also mentions that the role of gas ‘peakers;’ in supporting wind and solar is now being challenged by battery storage. It states that the role of gas in providing flexible generation to support variable renewable energy via peaker plants, “is being challenged, in some respects, by increasing investments in battery storage and grid management capabilities, which – if brought to scale – could fulfill the same short-term flexibility functions as gas.” It’s a cautious but clear recognition that gas is not only losing ground to wind and solar for so-called baseload, but also to batteries and smart grid technology for peaking and other grid balancing services.

When it comes to China and India, the world’s most prolific users of coal, the report also makes clear that gas struggles to compete for market share against both coal and renewable energy. This is because most gas is imported by pipeline or shipped as LNG, and that’s expensive. The future of gas in either market is limited by its high cost, and wind and solar are the main technologies competing with coal in those countries. We will discuss gas use in sectors other than power in subsequent blogs.

These two areas of the report, showing the impotence of gas in reducing emissions, and the crumbling economic case for new gas-fired power generation, reiterate the main theme in our burning the gas bridge fuel myth report. That is that contrary to the claims of industry and many in government, gas is not clean, cheap or necessary.

The fact that renewables are now able to provide large amounts of electricity cheaper than coal or gas has changed the expectation that large amounts of new gas power capacity will be added in the future. Indeed, in the mature power markets of Europe and North America, gas-fired capacity is generally underutilized as cheaper renewables are prioritized, and coal subsidies and regulatory protections keep some coal plants on life support. This leads to the report’s main policy recommendation, which is to implement carbon pricing in the U.S. and raise carbon prices in Europe in order to encourage coal-to-gas switching and raise the utilization rates of these underused gas plants.

As we’ll see in part 2, this is a deeply flawed policy prescription with huge risks for the climate. Not least because of the dangers of locking in gas production and infrastructure. This is an issue the report pays lip service to, but then ignores in the discussion of this policy recommendation.

So while this report appears to acknowledge the limited role of gas in reducing emissions, highlights the weak economic case for adding new gas power capacity, and warns of the climate risks of locking in gas use, all examples of refreshing honesty on gas at the IEA, it then curiously goes on to make a case for more gas. We’ll look at the issues with the analysis in the subsequent blog posts later this week.

* Structural economic changes are mostly changes in the energy intensity of economic activity. For example reductions in energy intensive manufacturing such as steel production.

Read Part II in this series: “The IEA’s plan to increase gas consumption locks in climate chaos.”

For more on gas and climate go to priceofoil.org/gas

Also see: The IEA’s plan to increase gas consumption locks in climate chaos

Superb analysis/